Bare Bone Basics: The Limited Partnership Agreement

What are some important contractual terms to be aware of?

In this post, we’ll dive into the basics of a limited partnership agreement (LPA) and a few of the key terms that shape the relationship between fund managers and investors in a private fund.

An LPA is the governing document for a fund structured as a limited partnership—a legal entity that has long been the favorite of venture capital, hedge, and private equity funds in the United States. And though the LPA might not forthrightly feature anything weird like a purple ostrich swimming in the Atlantic, it’s filled with esoteric details that can sometimes feel as rarefied as a flightless bird in the surf.

But we shall begin with more fundamental, straightforward terms.

Limited Partnerships: An Introduction

A limited partnership consists of at least two types of partners: one general partner (GP) and one or more limited partners (LPs). The GP holds broad liability for the fund’s assets. Meanwhile, the LP’s liability is capped at the amount it commits to the fund—similar to shareholders in a corporation, who aren’t personally responsible for the company’s debts and obligations beyond their investments.

On the flip side, the GP also enjoys broad discretion over the management of the fund’s assets. They’re in charge of the ship. The LPs, however, occupy a passive role in the backseat—unless, of course, a few key decisions pop up that require their approval. This could include things like extending the fund’s life or approving an amendment to the LPA, typically through an advisory committee made up of other limited partners. So some LPs have a say in a handful of critical matters, but they’re far from calling all the shots.

Why has the limited partnership structure earned its place as the preferred choice among fund managers in the United States? Well there are many reasons, but here are two commonly cited ones:

Tax Benefits: Limited partnerships enjoy “pass-through” taxation. This means that the fund itself doesn’t pay taxes on its income. Instead, the tax liability passes through to the partners, who are taxed only once on their share of the income distributions—unlike a typical corporation, which gets taxed at both the entity and shareholder levels.

Contractual Flexibility: Limited partnerships allow for a tailored approach to structuring both the economic and management rights within the fund. Some people—like the fund’s founder—might hold both economic and management rights. Others—like LPs—typically only hold economic rights, while individuals like salaried investment professionals may only have management rights, with no entitlement to profits.

It is hardly surprising that over the years, the limited partnership structure has been the subject of much academic debate, case law, and treatises.

That said, newer structures have gained traction, notably the limited liability company (LLC), originated by the Wyoming state legislature in 1977 thanks to some creative lobbying by the Hamilton Brothers Oil Company. LLCs allow for more flexibility in structuring management rights, vesting them in multiple “members” (the LLC equivalent of partners), without the risk of unlimited liability. Like limited partnerships, LLCs also benefit from a pass-through tax structure.

However, despite the rise of these newer options, the limited partnership benefits from inertia. It’s the good ol’ reliable of fund structures, beloved for its stability and its well-understood mechanics.

Economic vs. Managerial Terms

In prior posts, we touched on the importance of ambition and desire. In many ways, an LPA embodies these qualities. It serves as both a playbook and a novel—an entrepreneurial framework that enables professional money management while intertwining the fates of capital allocators and seekers.

However, the value of an LPA lies not just in individual terms, but in the relationships between them. For example, the managerial rights of a GP are shaped by the rights granted to LPs.

Naturally, LPAs are highly confidential, and analyzing them for quantitative patterns is a challenge—despite advancements in data analytics. However, by approaching the LPA as a collection of “economic” and “managerial” provisions, we can start to make sense of its complexities.

Economic provisions cover key matters like fees, expenses, and profit distributions, while managerial provisions address governance issues such as key person clauses, tax elections, and cybersecurity measures.

At its core, the purpose of an LPA is clear: it memorializes the terms on which a capital allocator agrees to invest, and in doing so, nurtures the ambition of both parties.

Economic Terms

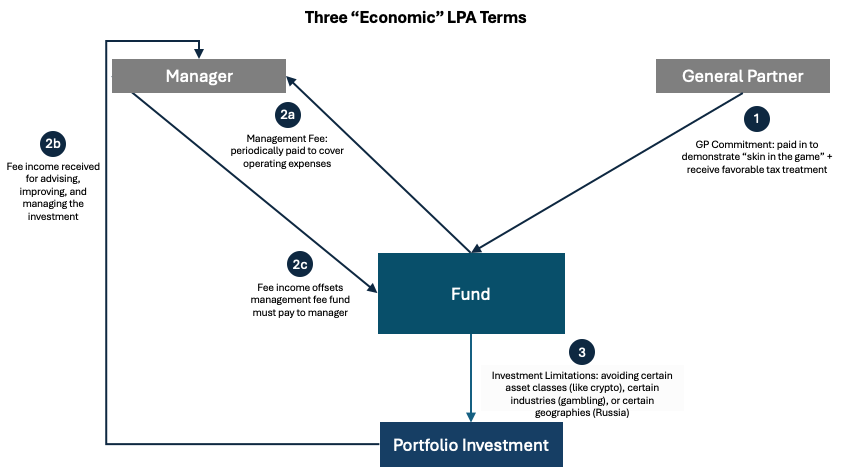

For starters, we can limit our discussion to three economic LPA terms and three managerial ones, as depicted below, so it’s not too overwhelming—along with some notes for each.

As a general note, a separate investment manager entity is often set up to collect the management fees is important for several liability, tax, and executive compensation reasons. Here’s a good LinkedIn post that explains why.

GP Commitment: A GP commitment refers to the capital that the GP personally invests alongside LPs in the fund. This is typically a small percentage of the total fund size, often ranging from 1% to 5%. LPs will often look to see if the GP is required to contribute its capital at the same time and on the same terms as they do, and whether it makes that contribution in cash. If not, they may ask: what percentage of the GP commitment can be paid through a management fee waiver? A waiver allows a fund manager to forgo fees in exchange for a share of the fund’s profits. This increased share may qualify as a “profits interest” under IRS rules, enabling the GP to defer taxes on the income and eventually pay them at the lower capital gains rate when the income is recognized. If management fee waivers are permitted, LPs may also ask whether the GP is required to bear any expenses, fees, or penalties imposed by the IRS if the waiver is challenged.

Management Fees:

(a) Management fees are perennial negotiatory favorites. These fees compensate the GP for managing the fund, typically ranging from 1.5% to 2.5% of committed capital during the investment period (usually the first 5 years). After this period, the fee often shifts to a lower percentage based on invested capital or net asset value. This transition reflects the reduced need for active capital raising as the fund moves into the later stages of investing and managing portfolio companies. As mentioned above, waivers are sometimes granted, where the GP waives part or all of the management fee in exchange for a larger share of carried interest or equity in the fund.

(b) Additionally, the fund may receive various types of fee income from its portfolio companies, including transaction fees (for arranging or advising on deals), monitoring fees (for overseeing portfolio management), and management fees (for providing management services to the company).

(c) To align interests with LPs and reduce the overall cost to the fund, these portfolio company fees are sometimes used to offset management fees at the fund level. In other words, these fees can be credited toward reducing the management fee charged to LPs.Investment Guidelines and Restrictions: This is a vast topic that has economic and managerial/governance components, but the spirit of the concerns involved are driven chiefly by economics, so I figured it would be better to include this discussion here rather than in the next section. Some important questions:

Are non-control positions permitted (for traditional PE funds, for example)?

Are investments in digital assets permitted? If so, how will those assets be liquidated as part of the return of profits?

Are investments in public securities permitted (for PE/VC)? If so, is there a cap on public securities as a percentage of capital commitments (typically no more than 5%)?

Are illiquid investments permitted (for a hedge fund)?

Is there a geographic mandate?

Does the LPA include GP undertakings to comply with anti-money laundering laws or relevant foreign counterparts?

Are investments in other funds permitted?

Does the LPA permit follow-on investments or recycling of profits as part of a reinvestment? If so, are these figures capped at 20% of aggregate capital commitments?

Managerial LPA Terms

Managerial terms are crucial because they define the decision-making structure and operational controls of the fund, ensuring that economic provisions—such as profit-sharing, distributions, and capital commitments—are effectively implemented, while aligning the interests and responsibilities of GPs and LPs.

Investment Allocation Policies: These policies govern how the GP divvies up investment opportunities between the fund, co-investors, and others. They aim to ensure transparency and fairness, and to avoid any awkward “who gets what” moments. LPs will often ask whether the GP and any other relevant parties (like the manager) are required to offer all suitable investment opportunities to the fund. These policies heavily consider the amount of discretion the GP has in determining whether an investment opportunity is “appropriate” for a fund.

Sometimes, a manager may establish an executive fund, typically reserved for the GP, key insiders, or executives, allowing them to co-invest alongside the main fund. LPs will often ask if the executive fund is required to invest pari passu (on substantially the same terms and same time) with the main fund.

Key Person Events: This provision protect the fund from the loss of its crucial team members, such as founders whose reputations are critical for an LP’s decision to commit money to the fund. If one of these key persons exits—whether by leaving the firm or through death/incapacitation—the fund may pause, or even trigger a vote among LPs. This ensures the fund doesn’t lose direction or momentum if top talent departs.

LPAC (Limited Partner Advisory Committee): The LPAC acts as the fund’s unofficial board of advisors, made up of larger LPs who are involved in decisions concerning conflicts of interest, fund life extensions, or valuations—some of which require notice and others full approval. LPs often have questions:

Is there a cap on the number of LPAC members?

Is a GP affiliate permitted to be on the LPAC?

Can LPs hold a meeting without the GP’s representatives for certain voting matters (the GP doesn’t always grant this right)?

Are LPAC members indemnified, apart from bad faith actions?

Is there a budget for separate LPAC legal counsel?

There’s so, so much more than what appears in these graphs.

We will build on these terms in the future. And perhaps catch a purple ostrich in action!

Fee offsets are one of those sneaky terms that look harmless but can actually be somewhat insidious. Fees can generally only be offset to the extent that management fees are being generated (and offsets can be carried forward). However, near the end of a fund's life (>Year 10), when management fees are no longer being generated, all those fees just go straight to the GPs bottom line because there is nothing to 'offset' them against.

Don't the GP also get some kind of incentive based compensation fee in addition to their standard management fee? I think the incentive based compensation is usually a percentage of both the realized and unrealized gains the fund earns on an annual basis. Or am I thinking about something else?